BTO Flat or New Condo, Which Should a First-Timer Invest In?

It’s no secret that as an asset class, real estate performs exceptionally well in Singapore.

Not only does it tick off all of the boxes on what makes an investment worthwhile – such as having low volatility, growth consistency, and potential for wealth generation – buying a property of your own also satisfies the basic human need of having a roof over one’s head.

For these reasons alone, purchasing a home makes absolute sense, be it for ownership or investment purposes. The question then is: given the option, which should you buy for your first home, an HDB flat or a new launch condominium?

Comparing between BTO Flats and New Condominiums as first homes

The modus operandi of most Singaporean couples who aspire to home ownership goes something like this. Get married, apply for a Build-to-Order (BTO) flat next, and then wait for the keys to their first home.

Though this is indeed the ‘customary’, and likely, the most frequently taken path by first-time buyers towards residential property ownership locally, there are other roads open too.

Other than entering the resale home market, aspiring homeowners can opt to purchase a new condominium as well – which could prove to be the ideal choice for certain segments of buyers due to the upsides involved.

To help you arrive at a decision, here’s a quick comparison between BTO flats and newly-launched condominiums across all aspects of the home ownership experience in Singapore – from buying to selling, and more.

1. Buyer competition and eligibility

Putting matters of cost aside, a new launch condominium could prove to be more accessible to first-time homebuyers in Singapore due to the challenge of balloting for a BTO flat.

One does not have to look hard to find reports in mainstream media about oversubscribed estates (see here, here, and here) or even anecdotal accounts of unsuccessful application attempts, like this couple who failed 13 times in their bid for a BTO flat, which suggest that there could be some truth to this claim.

Furthermore, to be eligible for a BTO flat, buyers are required to meet specific conditions set forth by HDB. For instance:

- The owner(s) has to qualify under one of the BTO flat eligibility schemes. (e.g. Public scheme, Fiancé/Fiancée scheme, Single Singapore Citizen scheme)

- At least 1 of the applicants for a BTO flat must be a Singapore citizen and one other being a citizen OR a Permanent Resident.

- Both applicants must be at least 21 years of age OR 35 if they are single or divorced.

In addition to the above, there are also stipulated income ceilings for different flat types, rules concerning the ownership of private property – the list goes on.

Understandably, these conditions are in place to ensure that BTO flats are sold to the people who need them most, but for those looking for a more straightforward route towards home ownership, perhaps entering the private housing market is the way to go.

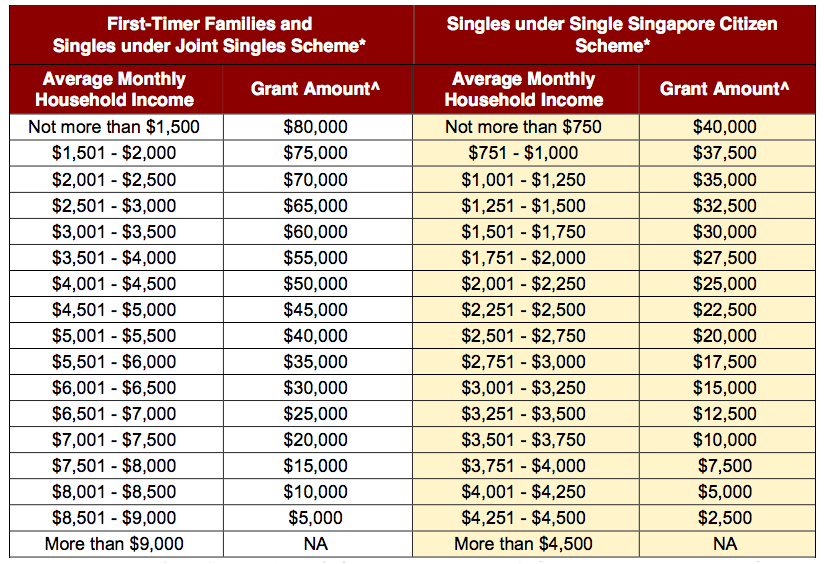

2. Housing grants

When it comes to financial assistance, homebuyers who are in need will do well to purchase a BTO flat due to the Enhanced Housing Grant (EHG) available to first-timers.

Depending on their household’s average gross monthly income (derived over 12 months before the submission of a BTO flat application), it’s possible for a homebuyer to receive up to $80,000 in grants. The monies received from the EHG will help make a BTO flat more affordable as they can be used to ‘reduce’ the price of the property, and hence mortgage size.

A breakdown of EHG amounts that homebuyers can possibly receive based on household income level is as follows:

Needless to say, first-timers who are purchasing a new launch condominium won’t be able reap the benefits of the EHG – though there are other advantages that they’ll benefit from, such as…

3. Mortgage affordability

Generally speaking, first-time buyers of condominium homes are likely to enjoy higher mortgage affordability than their counterparts who have chosen to get a brand-new BTO flat.

Why that’s the case is due to the current rules governing property loans given by financial institutions in Singapore. They’re namely the Total Debt Servicing Ratio (TDSR) and the Mortgage Servicing Ratio (MSR), which help ensure that homebuyers aren’t borrowing beyond their means.

MSR caps the amount that borrowers can spend on mortgage repayments for a BTO flat to 30% of their gross monthly income, whereas TDSR has a higher (read: more lenient) threshold of 55% for loans on private properties instead.

This is a factor that first-timers should definitely consider when deciding between buying a BTO flat and a new condominium because it has a bearing on the maximum amount that they can take on a mortgage – and by association, the size and/or value of properties that they can afford.

4. Ease of unlocking property’s value

By and large, compared to those who have bought a BTO flat, owners of new launch condominiums have a shorter runway when it comes to unlocking the value of their homes.

Due to the Minimum Occupation Period rule, which restricts owners from selling or renting out an HDB flat within the first few years of moving in, they’ll only be able to profit and/or generate passive income from their property 5 years down the road.

In comparison, first-timers who have purchased a condo are free to sell or let their home to others almost immediately after getting the keys – with the only qualm being the Seller’s Stamp Duty (of up to 12%) that’s only levied on private properties sold within 3 years of their purchase.

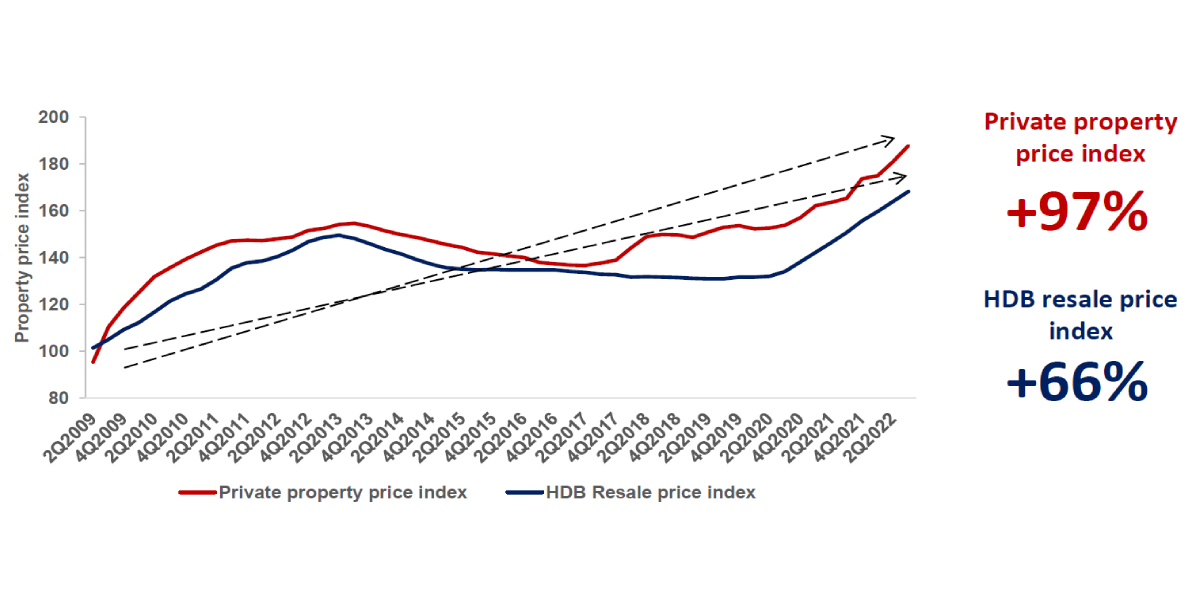

5. Profitability

Last but not least, the biggest case for buying a new-launch condominium over a BTO flat is profitability. Proof of the pudding: the respective price growths for private property and HDB resale flats from 2009 to 2022.

Across the past 13 years, the private property price index saw a 97% increase in value, whereas the HDB resale price saw a 66% rise – which though impressive, is almost a third less than the growth its counterpart has experienced.

Source: URA, HDB, ERA Research and Consultancy

So, if wealth generation is your key objective as a homebuyer, the choice is pretty clear.

To sum up

In summary, the question of whether to purchase a BTO flat or a new launch condominium as a first home is best answered by what you’re looking out for.

Assuming all other things are equal, if generating wealth and cash flow are your primary goals, purchasing a new private home is probably the wise choice. Otherwise, if having long-term and affordable accommodation is your priority, then a BTO/HDB flat would likely to be a better fit.

Still can’t decide? Feel free to speak to one of our trusted ERA advisors for more advice!

Disclaimer for consumers

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salespersons accept no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.